2. An alternative possibility: the relative MAGNITUDE of military spending simply has become too small for the GROWTH of military spending to matter. To put this process in context, note that, by the mid 1990s, the size of U.S. exports to developing Asia alone had already surpassed U.S. military procurement. See Will Re-Armament Wreck the 'Asian Miracle'? (1987), Chart II.6 on page 18 http://bnarchives.yorku.ca/152/01/970301N_Will_rearmament_wreck_the_Asian_miracle.pdf

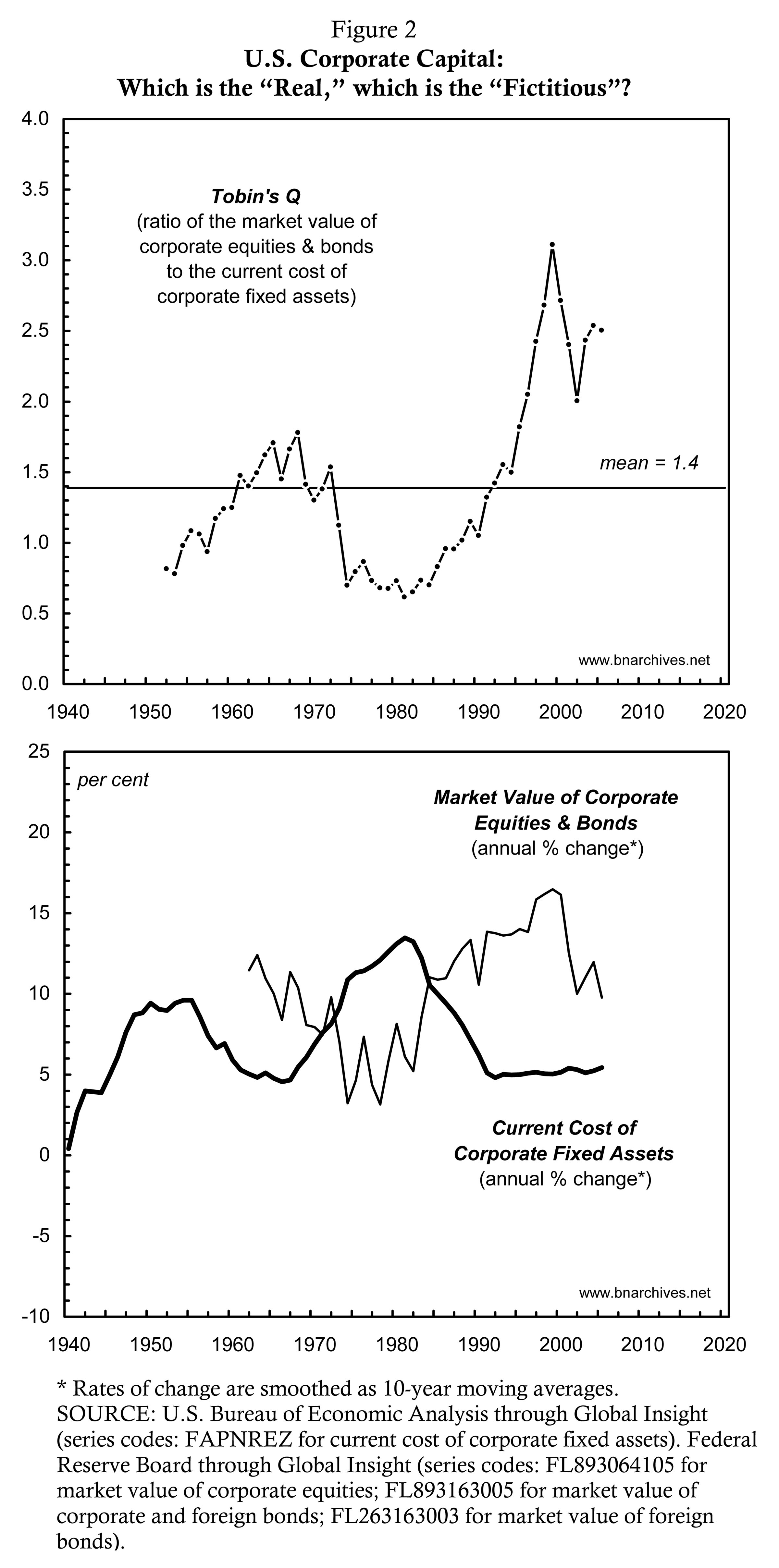

3. A third possibility: our continuous preoccupation with the "real economy" diverts our attention from the real process of financial capitalization -- to the obvious joy of the accumulators http://bnarchives.yorku.ca/215/04/20061027_bn_elementary_particles_rm_transcribed_figure2.jpg

Jonathan

++++++++++++++++++++++++

Maybe this is a short-term observation - an occupational hazard of covering Wall Street - but the relation seems to have broken down after 1990. The military share fell during the Clinton years and growth rose; the reverse has been true in the Bush years. I wonder if this has anything to do with the composition of military spending, which is decreasingly about mass-produced industrial goods (which presumably have a higher multiplier) and increasingly about specialized high-tech gear, R&D, and purchased services (with presumably lower multipliers).

Doug

{kind=link}